Levy arrears are not an administrative inconvenience. They are a legal and financial threat to every owner in your scheme. When one owner stops paying, the compliant owners carry the shortfall, and trustees who fail to act may be in breach of their fiduciary duty. If your body corporate is dealing with unpaid levies, this guide sets out exactly what the law requires and what to do about it.

Why Unpaid Levies Are a Legal Emergency, Not a Cash Flow Problem

Section 3(1)(c) of the Sectional Titles Schemes Management Act 8 of 2011 (STSMA) places a clear obligation on the body corporate to require owners to make contributions to its funds whenever necessary. This is not a discretionary power. It is a statutory duty.

Trustees who delay collection are not being kind. They are exposing the body corporate to financial instability, deferring maintenance, depleting reserve fund contributions, and potentially breaching their fiduciary duty to compliant members. We have seen this pattern hundreds of times since we began working with bodies corporate in 2002: early inaction turns a recoverable debt into a crisis.

The law is on the body corporate's side. Use it.

For a broader understanding of the governance framework that underpins levy collection, read our post on body corporate rules in South Africa before proceeding.

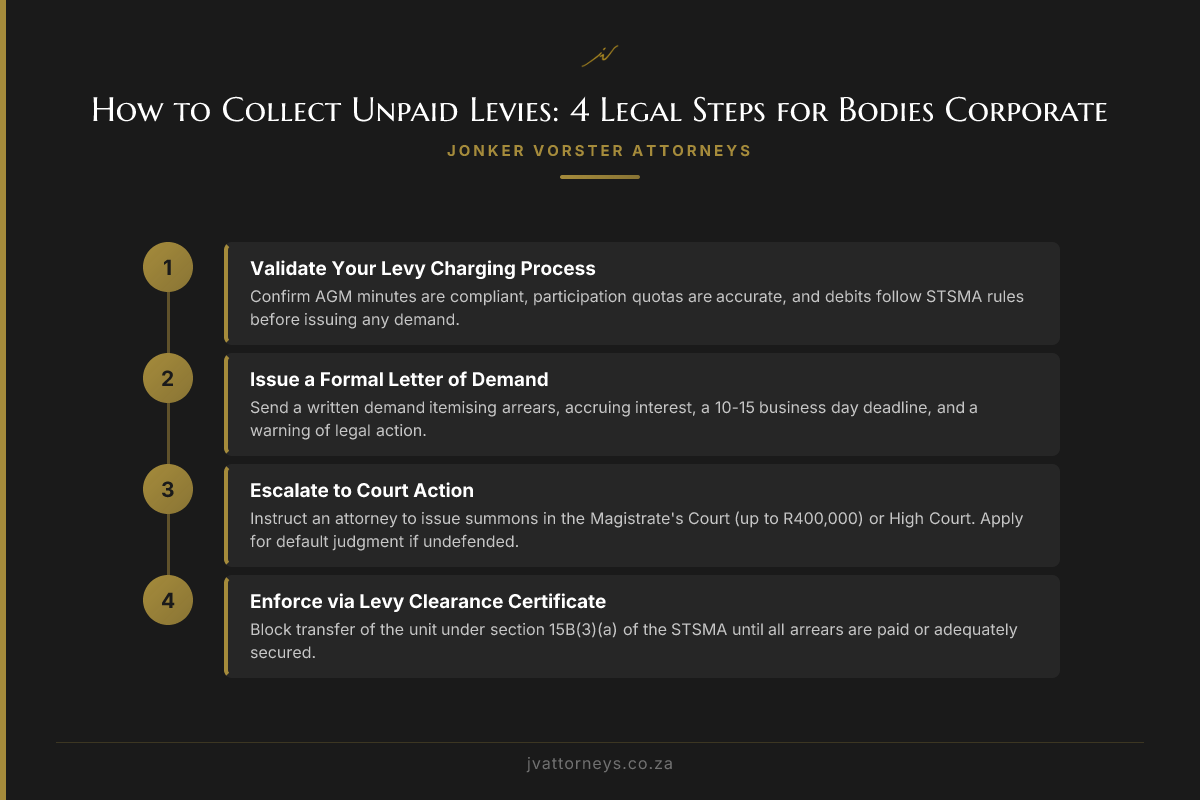

Step 1: Get Your Levy Charging Process Right Before You Collect

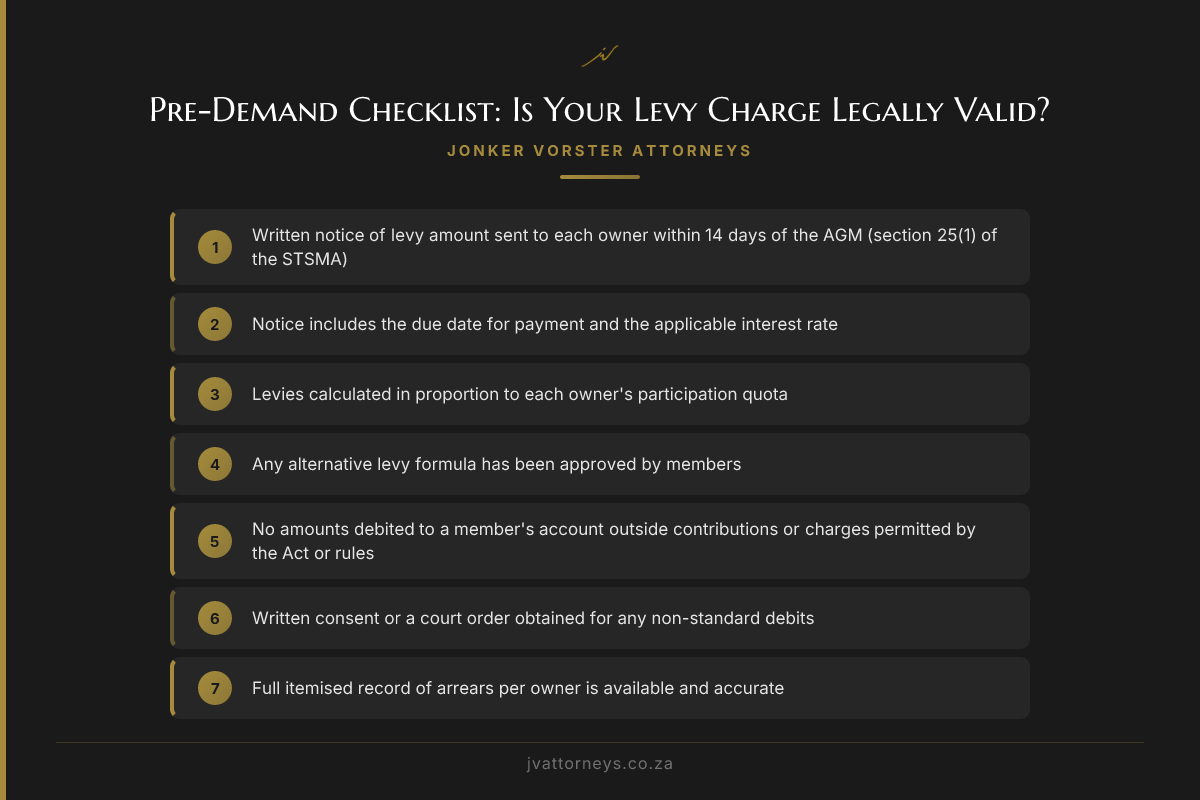

The most common reason levy collection efforts fail is not debtor resistance. It is defective charging. A defaulting owner's first line of defence is to challenge whether the levy was validly raised in the first place.

Before issuing any demand, trustees must confirm the following:

- Proper AGM minutes: Section 25(1) of the STSMA requires the body corporate to send each owner written notice of the levy amount, the due date for payment, and the applicable interest rate within 14 days of the annual general meeting.

- Accurate participation quota: Levies must be calculated in proportion to each owner's participation quota (or another formula approved by members), not by flat rate unless the rules specifically permit it.

- Correct debiting: Management Rule 25(5) of the STSMA is unambiguous: the body corporate must not debit a member's account with any amount that is not a contribution or charge levied in terms of the Act or the rules, without the member's written consent or the authority of a court order. Any amount debited outside this framework is vulnerable to challenge.

If your scheme's charging process has gaps, fix them before you pursue collection. A demand built on a defective levy invoice process will not survive scrutiny. Our post on protecting your estate against levy charge disputes covers the preventive side of this in more detail.

Step 2: Issue a Formal Letter of Demand

Once you have confirmed the levy is validly charged, the next step is a formal letter of demand addressed to the defaulting owner.

A compliant letter of demand must include:

- The full amount outstanding, itemised by month

- The interest accruing on the arrears (at the rate approved at the AGM)

- A reasonable payment deadline (typically 10 to 15 business days)

- A clear statement that legal action will follow if payment is not received

The letter can be issued by the trustees, the managing agent, or an attorney. In our experience, a letter issued on an attorney's letterhead produces a significantly higher response rate than one from the managing agent alone. It signals that the body corporate is serious and that the next step is court.

This step also creates the documented paper trail that courts expect. Interest begins accruing from the date of default, and the demand letter establishes that date clearly in the record.

Step 3: Escalate to Legal Action via Magistrate's Court or High Court

If the demand goes unanswered, the body corporate must proceed to formal legal action. The process is:

- Summons: An attorney issues summons in the appropriate court. For debts up to R400,000, the Regional Court has jurisdiction. For larger amounts, or where the matter involves complex legal issues, the High Court is the appropriate forum. If you are unsure which court applies to your specific debt, seek legal advice before proceeding.

- Default judgment: If the owner does not defend the matter, the body corporate applies for default judgment. For undefended matters, this is typically the most efficient route.

- Enforcement: Once judgment is obtained, the body corporate can enforce it through a range of mechanisms, including a garnishee order (attaching the debtor's salary or bank account) or attachment and sale of movable assets. In serious cases, the body corporate can apply for the unit to be sold in execution. Read our post on whether the body corporate can sell your property for unpaid levies for a full explanation of that process.

We handle 450+ contested matters per year and process 10,000+ debt recovery matters annually. For undefended levy collection matters, our average resolution time from instruction to outcome is approximately 6 - 9 months.

Step 4: Use the Levy Clearance Certificate as a Recovery Safeguard

Even where immediate enforcement is not possible, the body corporate holds a powerful backstop: the levy clearance certificate.

Under section 15B(3)(a) of the STSMA, the Registrar of Deeds cannot register the transfer of a sectional title unit until the body corporate has issued a certificate confirming that all levy arrears have been paid or adequately secured. In plain terms: a defaulting owner cannot sell their unit and walk away from the debt.

This provision means that even if enforcement takes time, the body corporate will recover what it is owed at the point of sale. Hendré Vorster, our co-founder and an admitted conveyancer since 2008, deals with this intersection of levy recovery and property transfer regularly. The levy clearance certificate is not a passive document; it is an active enforcement tool.

For a detailed explanation of how the certificate works and when it is required, see our post on the levy clearance certificate.

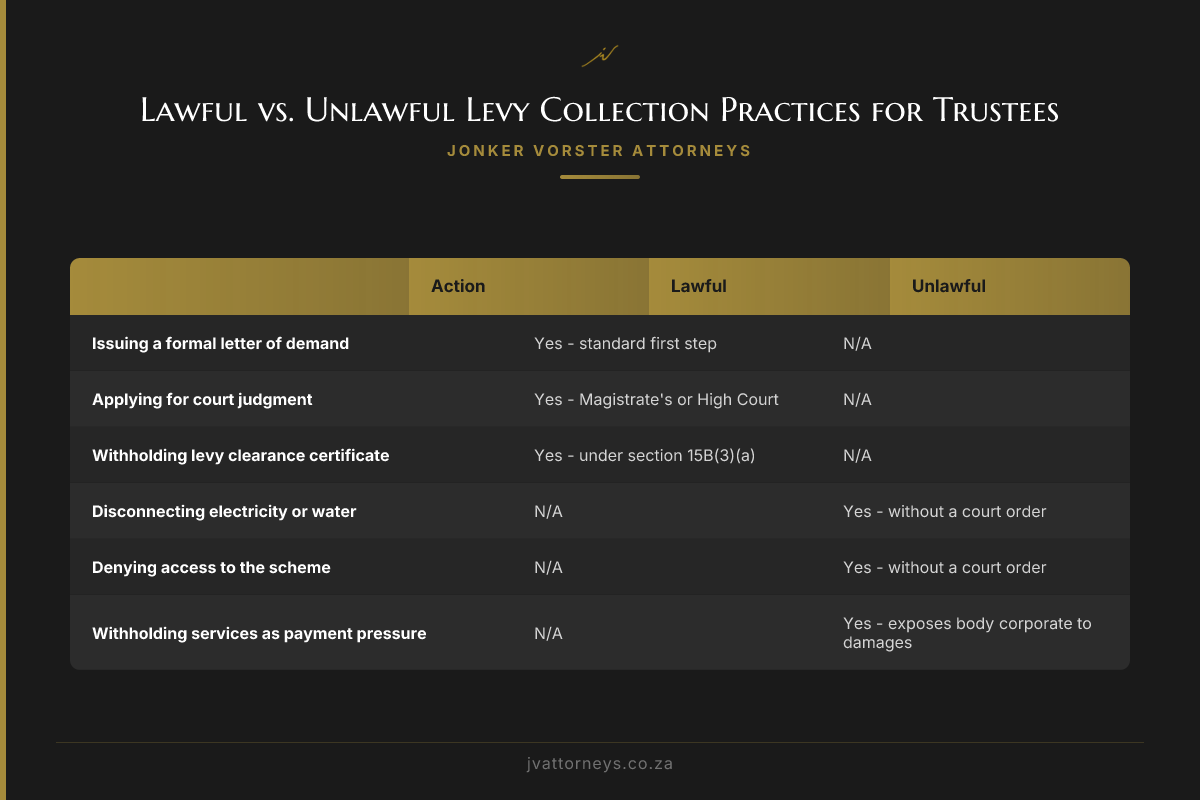

What Trustees Cannot Do: Unlawful Collection Practices to Avoid

This section is not optional reading. Trustees must understand the boundaries of lawful enforcement.

Regardless of the amount owed, the body corporate may not (without a court order):

- Disconnect or restrict the supply of electricity, water, or gas to the defaulting owner's unit

- Deny the owner or their tenants access to the scheme or common property

- Remove or withhold services as a form of pressure to pay

Multiple High Court judgments have confirmed that these actions are unlawful, even where the arrears are substantial. Trustees who authorise disconnections or access restrictions expose the body corporate to urgent interdict applications, damages claims, and significant legal costs.

The body corporate's only lawful remedies are formal legal processes: demand, court action, and arbitration. There are no shortcuts, and attempting to create them creates liability.

How Jonker Vorster Attorneys Helps Bodies Corporate Recover What They Are Owed

Jonker Vorster Attorneys has been working with bodies corporate and HOAs since 2002. Over more than two decades, we have built an integrated recovery model that combines pre-legal debtor management with legal enforcement, reducing both the time to recovery and the administrative burden on trustees and managing agents.

Here is how our process works:

Pre-legal phase: Through our integration with Jumping Fox Software, a cloud-based debtor management platform co-founded by our directors, levy accounts are monitored automatically. Automated payment reminders, credit bureau checks via TransUnion, Experian, and VCCB, and compliance tracking happen before a matter ever reaches our desk. Credit bureau listings are a genuine deterrent that no competitor in this space currently uses as systematically as we do.

Electronic handover: When pre-legal efforts are exhausted, instructions transfer electronically from Jumping Fox Software to our legal team. There is no manual re-capturing of information, no delay, and no gap in the paper trail.

Legal recovery: Depending on the quantum and complexity of the matter, we proceed via the Magistrate's Court, or the Cape Town High Court (Western Cape Division). We act in courts across Paarl, Stellenbosch, Wellington, and the broader Western Cape, as well as nationally via correspondent attorneys.

No Success, No Fee: For qualifying levy collection matters, we operate on a No Success, No Fee basis. The body corporate carries no upfront legal cost risk.

Whether your scheme is in Paarl, Stellenbosch, or anywhere in South Africa, our levy collections service is built to recover what your scheme is owed, efficiently and lawfully.

For a related overview of the recovery process, see our post on recovering outstanding levies.

This article is intended for general informational purposes only and does not constitute legal advice. For advice specific to your situation, please contact Jonker Vorster Attorneys directly.

Frequently Asked Questions

Yes, South African law does not always require a formal letter of demand before summons is issued. However, it is strongly advisable and is standard practice in levy collection matters. A letter of demand gives the defaulting owner a final opportunity to pay, creates a documented paper trail, and demonstrates good faith to the court.

For undefended levy collection matters handled by a specialist attorney, Jonker Vorster Attorneys' average resolution time is approximately 6 months from instruction to outcome. Defended matters, or those requiring execution against immovable property, take longer.

Yes, in serious cases. Under section 15B(3)(a) of the Sectional Titles Schemes Management Act 8 of 2011, a unit cannot be transferred until all levy arrears are settled or adequately secured. If a judgment is obtained and the owner does not pay, the body corporate can apply to court for the unit to be sold in execution.

No. Disconnecting electricity, water, or gas, or denying access to the scheme, is unlawful regardless of the amount owed. Multiple High Court judgments have confirmed this position. The body corporate's only lawful remedies are formal legal processes: demand or court action.

The interest rate on overdue levies must be approved by members at a general meeting and applied uniformly to all defaulting owners. Trustees cannot set the rate unilaterally. The rate and the method of calculation must be properly documented and consistently applied to withstand challenge.

A levy clearance certificate is a document issued by the body corporate confirming that all levy arrears on a unit have been settled or adequately secured. Under section 15B(3)(a) of the STSMA, the Registrar of Deeds cannot register the transfer of a sectional title unit without this certificate. It is required at the point of sale.